Ever felt like your credit score is a mysterious cipher, holding the key to financial freedom but speaking a language you just can’t quite decode? It’s more than just a three-digit number; it’s a potent symbol of your financial responsibility, influencing everything from loan approvals to interest rates on that shiny new car (or even your rental application!). But fear not, financially curious explorer! This article dives deep into the numerical jungle of your credit score, unraveling the secrets behind each digit. Prepare to decode the enigma, understand its impact, and ultimately, take control of your financial destiny. Let’s embark on a journey to demystify the digits, transforming that number from a source of anxiety to a tool for empowerment.

Table of Contents

- Unveiling the Mystery Behind Your Three Digit Reputation

- Beyond the Number: Examining the Factors That Shape Your Score

- Navigating the Credit Score Landscape: A Guide to understanding Key Influencers

- Boosting Your Creditworthiness: Practical Steps for a Better Financial Future

- Long Term Credit Health: Building a Strong Foundation for Sustained Success

- Q&A

- The Conclusion

Unveiling the Mystery Behind Your Three digit Reputation

Ever wondered what that elusive three-digit number says about you? It’s more than just a score; it’s a key that unlocks financial opportunities, or slams the door shut. Understanding exactly what influences it is the first step towards wielding its power. Think of it as your financial report card, meticulously graded based on your borrowing habits and repayment prowess.

but what’s actually *in* that report card? Lenders are looking at a few key areas to determine your creditworthiness. Let’s break down the factors that heavily influence decoding your creditworthiness:

- Payment History: This is the big one! Have you consistently paid your bills on time? Delinquencies can significantly impact your score.

- Amounts Owed: How much of your available credit are you using? Maxing out credit cards sends a red flag.

- Length of Credit History: A longer track record generally indicates lower risk to lenders.

- Credit Mix: Showing responsible management of different types of credit (credit cards, loans, etc.) can be beneficial.

- New Credit: Opening too many new accounts in a short period can temporarily lower your score.

Knowing your score is important, but understanding the underlying reasons behind that number is even more crucial. different scoring models exist, and each assigns slightly different weights to these factors. Let’s look at one popular, albeit fictional, example.

| Factor | Weight (Example) | Impact |

|---|---|---|

| Payment History | 35% | Major |

| Amounts Owed | 30% | Significant |

| Credit Age | 15% | Moderate |

| Credit Mix | 10% | Minor |

| New Credit | 10% | Minor |

Don’t just be a number. Take control of your financial narrative by understanding the pieces that compose your credit rating, and actively work to improve them. building good credit is a marathon, not a sprint!

Beyond the Number: Examining the Factors That Shape Your Score

Ever wonder why your credit score is the number it is? It’s not a random lottery; it’s a carefully calculated assessment based on your financial behavior. Think of it as a report card, but instead of grades in math and science, it showcases how reliably you manage credit. Understanding the levers that influence this score empowers you to take control and steer your financial destiny.

So, what goes into this mystical number? The most widely used scoring models consider several key components. These aren’t weighted equally; some factors carry more weight than others. Here’s a rapid rundown:

- Payment History: This is the big kahuna! Consistently paying bills on time is crucial.

- Amounts Owed: How much debt are you carrying compared to your available credit? High balances can signal risk.

- Length of Credit History: A longer, well-managed credit history is generally viewed favorably.

- Credit Mix: Having a variety of credit accounts (e.g.,credit cards,loans) can improve your score.

- New Credit: Opening too many new accounts in a short period can ding your score.

Let’s look at a quick hypothetical. Say you have two friends, Sarah and David. Sarah always pays her bills on time, has a low credit utilization, and boasts a long credit history. David, on the other hand, sometimes misses payments, carries high balances, and recently opened several new credit cards. You can probably guess who has the higher score!

| Factor | Sarah | David |

|---|---|---|

| payment History | Excellent | Fair |

| Credit Utilization | 10% | 75% |

| Credit Age | 10 years | 3 years |

Ultimately, your credit score is a dynamic snapshot of your financial responsibility. By actively managing the factors mentioned above, you can take steps to improve your score and unlock a world of financial opportunities. Remember, building good credit is a marathon, not a sprint!

Navigating the Credit Score Landscape: A Guide to Understanding Key Influencers

Imagine your credit score as a financial fingerprint,a three-digit number whispering tales of your past financial behavior to lenders. It’s more than just a number; it’s a key that unlocks opportunities, from snagging that dream home to securing a lower interest rate on your next car. Understanding the story behind that score empowers you to take control of your financial destiny. So, let’s peel back the layers and decode the meaning behind each crucial number, transforming the seemingly complex into simple, actionable knowledge.

The magic number, ranging typically from 300 to 850, is constructed from a blend of factors, each contributing its own unique weight. Think of it as a financial recipe, where ingredients like payment history, amounts owed, length of credit history, credit mix, and new credit are carefully measured and combined to bake your score. While the exact weighting varies by scoring model (like FICO and VantageScore), understanding the core ingredients is essential. here’s a quick rundown:

- Payment History: Have you consistently paid your bills on time? This is a HUGE deal!

- Amounts Owed: How much credit are you currently using compared to your available credit? Keeping balances low is key.

- Length of Credit History: The longer you’ve responsibly managed credit, the better.

- Credit Mix: Do you have a healthy mix of different types of credit, like credit cards and loans?

- New Credit: opening too many new accounts in a short period can ding your score.

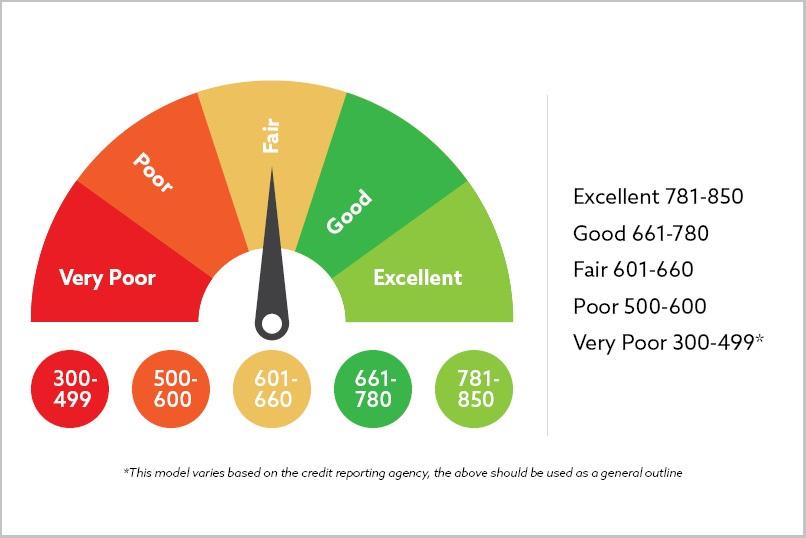

To truly understand the impact of each factor, let’s envision different score brackets and the typical borrower profiles associated with them. This allows you to benchmark yourself and identify areas for improvement. For presentation purposes, we will use FICO score below:

| Score Range | Rating | Typical Borrower Profile |

|---|---|---|

| 300-579 | Very Poor | Likely has a history of missed payments or serious delinquencies. |

| 580-669 | Fair | May have some past credit challenges, such as late payments. |

| 670-739 | Good | Generally makes payments on time and manages credit responsibly. |

| 740-799 | very good | Has a strong credit history with consistent on-time payments. |

| 800-850 | Exceptional | Demonstrates exemplary credit management and poses a low risk to lenders. |

Boosting Your Creditworthiness: Practical Steps for a Better Financial Future

Imagine your credit score as a financial report card.But instead of A’s and B’s, you have a three-digit number that whispers volumes about your borrowing habits. These numbers, ranging typically from 300 to 850, aren’t random. They’re calculated by credit bureaus using complex algorithms based on your credit history. Understanding what each range signifies is the first step in taking control of your financial destiny. Think of it as learning to decipher the language of lenders!

So, what exactly does your score reveal? Here’s a quick breakdown of the common scoring ranges and their implications:

- Exceptional (800-850): Welcome to the VIP lounge! You’re considered a low-risk borrower, granting you access to the best interest rates and loan terms.

- Very Good (740-799): You’re in excellent shape! Lenders view you favorably, increasing your chances of approval and competitive offers.

- Good (670-739): Solid ground.While you might not snag the absolute lowest rates, you’re generally considered a reliable borrower with good approval odds.

- Fair (580-669): Proceed with caution.This range could lead to higher interest rates and potentially limited loan options. Focus on improving your credit utilization and payment habits.

- Poor (300-579): Time for a credit makeover! This score indicates a history of credit issues, and you’ll likely face difficulty securing loans or credit cards. Rebuilding is crucial!

Beyond the ranges, understanding the factors influencing your score allows you to strategically improve it. Credit bureaus analyze five key areas: payment history (the most significant!), amounts owed (credit utilization), length of credit history, credit mix, and new credit. Consistently paying bills on time, keeping your credit card balances low, and demonstrating responsible credit management are pillars of good credit health.

| Factor | Impact | How to Score high |

|---|---|---|

| Payment History | High | Always pay on time! |

| Amounts Owed | High | Keep balances low. |

| Credit Age | Medium | Hold accounts! |

| Credit Mix | Low | Vary credit types. |

Long Term Credit Health: Building a Strong Foundation for Sustained Success

ever wondered what that elusive three-digit number says about you? Your credit score is more than just a random value; it’s a powerful financial tool, a key that unlocks opportunities, or unfortunately, a barrier that keeps you from achieving your goals. Understanding its components is the first step toward mastering your financial destiny. Think of it as a financial report card, reflecting your payment habits and responsible borrowing behavior. Let’s dissect this crucial number to understand what makes it tick.

Several factors contribute to your credit score, each carrying different weight. Here’s a breakdown of the major players:

- Payment History: The cornerstone! Late or missed payments significantly impact your score.

- Amounts Owed: How much debt you’re carrying relative to your credit limits (credit utilization).

- Length of credit History: A longer,well-managed credit history generally boosts your score.

- Credit Mix: Having a variety of credit accounts (credit cards, loans) can be a positive.

- New Credit: Opening too many new accounts in a short period can slightly lower your score.

Different scoring models exist (like FICO and VantageScore), but they all generally use a similar range.Here’s a simplified look at what your score typically means:

| Score Range | Rating | Interpretation |

|---|---|---|

| 300-579 | Poor | High risk; difficulty obtaining credit. |

| 580-669 | Fair | Subprime borrower; may face higher interest rates. |

| 670-739 | Good | Acceptable; likely to be approved for credit. |

| 740-799 | Very Good | Low risk; favorable interest rates. |

| 800-850 | Excellent | Lowest risk; best terms and rates. |

Knowing your score is just the beginning. Actively taking steps to improve it is crucial for long-term financial well-being. Consistently paying bills on time, keeping credit utilization low, and being mindful of new credit applications are all vital strategies. Building a strong credit foundation isn’t a sprint; it’s a marathon that requires patience and consistent effort. Think of this knowledge as empowerment – you now have the tools to shape your financial future and unlock the doors to a brighter tomorrow!

Q&A

Decoding Your Credit Score: What Each Number Means – Q&A

So,you’ve stared at that three-digit number,your credit score,feeling like you’re gazing into a crystal ball filled with financial futures.We get it. It can be perplexing! Consider this your decoder ring. let’s break it down:

Q: Alright,let’s cut to the chase. Why should I even care about my credit score? Is it just some arbitrary number banks use to judge me?

A: It’s more than just a judgy number! Think of it as your financial reputation, whispered on the wind to lenders. A good score unlocks doors to better interest rates on loans, credit cards, even apartment rentals. A lower score slams those doors shut, or at least makes you pay a premium to squeeze through. In essence, it dictates how expensive it is to borrow money, and sometimes, even live your life.

Q: Okay, so borrowing money more cheaply sounds good. But how is this mysterious number actually calculated? It feels like magic!

A: It’s not magic, though wielding its power can feel pretty magical! The score is compiled using information from your credit reports, provided by credit bureaus. Imagine a panel of judges scrutinizing your financial habits, based on five key categories:

Payment History (35%): Do you pay your bills on time, every time? This is the biggest piece of the pie.

Amounts Owed (30%): How much debt are you carrying, and what percentage of your available credit are you using?

Length of Credit History (15%): How long have you been responsibly managing credit? A longer track record is typically better.

Credit Mix (10%): do you have a healthy mix of credit accounts, like credit cards, installment loans (car, mortgage), and other types of credit?

New Credit (10%): How often are you applying for new credit? Applying for too much credit in a short period can raise red flags.

Q: ”Amounts Owed” sounds tricky. Does that mean I should just avoid using credit cards altogether to keep that number low?

A: Interestingly, not using credit cards at all can actually hurt your score! Credit scores are based on showing responsible credit usage. The sweet spot is generally keeping your credit utilization (the amount of credit you’re using versus your total credit limit) below 30%. So, use your cards, pay them off regularly, and avoid maxing them out.

Q: What’s the point of “Credit Mix”? Do I actually need a mortgage to boost my score?

A: Absolutely not! A mortgage isn’t a prerequisite to climbing the credit score ladder. ”Credit Mix” simply indicates to lenders that you can responsibly manage different types of credit. A healthy mix can include credit cards and a personal loan, for example. Think of it as adding variety to your financial portfolio.

Q: Supposed I’ve made some mistakes in the past. Is my credit score doomed forever?

A: Not at all! Think of your credit score as a living document, constantly updating based on your financial behavior. Negative items, like late payments, do impact it, but they don’t last forever.Most negative information falls off your credit report after about seven years. Focus on building positive credit habits now* – paying bills on time, reducing your debt, and managing your credit accounts wisely. Over time, those positive actions will outweigh the past mistakes and help your score climb.

Q: Okay, this information is empowering. But what happens if I find errors on my credit report?

A: That’s a great question! Errors happen. It’s your right to dispute them. Contact the credit bureau directly (Equifax, Experian, and TransUnion) and provide documentation that shows the information is incorrect.They are legally obligated to investigate and correct any errors they find. Don’t let inaccurate information hold you back!

Q: what’s the single most important piece of advice you can give someone looking to improve their credit score?

A: Keep it simple: Pay your bills on time,every time,no exceptions. It’s the bedrock of a good credit score. Everything else is just icing on the cake. Make it a habit, set up reminders, automate payments… do whatever it takes to stay on top of your bills. Your financial future will thank you!

The Conclusion

So,there you have it. Your credit score, once a cryptic code, is now hopefully a bit more decipherable. Remember, this isn’t just a number; it’s a reflection of your financial story, a narrative you’re constantly writing with every purchase, bill payment, and financial decision. Understanding its language empowers you to edit, refine, and ultimately, control that narrative.Now go forth and write a financial story you’re proud of, one where your credit score sings a tune of responsible management and future opportunities. Consider this your translator; the rest is up to you. And who knows? Maybe one day, you’ll be the one decoding the mysteries of finance for someone else.