Ever feel like your hard-earned cash is just… sitting there? Like a precious gem gathering dust in a forgotten drawer? While keeping it safe is paramount, letting it stagnate means you’re missing out on potential growth. But plunging into the stock market might feel like diving into the deep end with no floaties.Enter the Money Market Account: a safe haven that’s more than just a holding pen for your funds.Think of it as a gentle, rippling pond – a stable, fluid environment where your money can slowly but surely accumulate value.This article will navigate you through the ins and outs of Money Market Accounts, helping you understand if they’re the perfect aquatic ecosystem for your financial flora and fauna.

Table of Contents

- Unlocking the Potential of Money Market Account Liquidity

- Demystifying Money Market account Interest Rate Fluctuations

- Strategic Use Cases for money Market Accounts Beyond Emergency Funds

- Navigating Fees and Minimum Balance Requirements for Optimal Returns

- Maximizing Your Money Market Account Strategy with Laddering Techniques

- Understanding the Tax Implications of Money Market Account Earnings

- Q&A

- To Wrap It Up

Unlocking the Potential of Money Market Account Liquidity

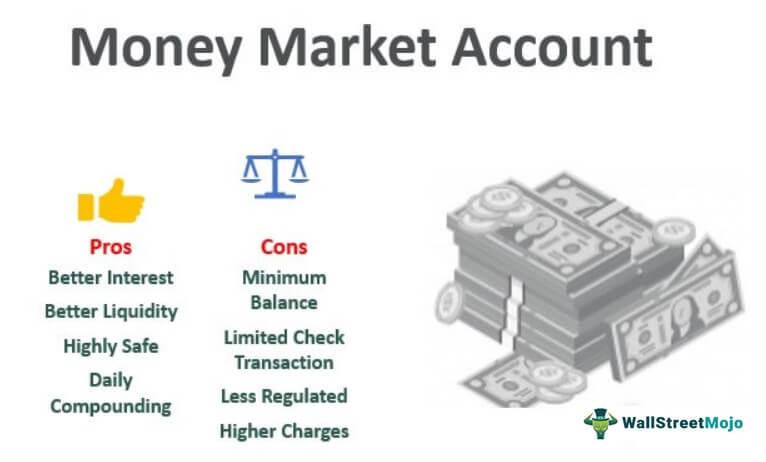

Ever dreamt of having your cake and eating it too? Money market accounts (MMAs) might just be the financial equivalent. They offer a sweet spot between the accessibility of a checking account and the growth potential of a savings account.Think of them as the Swiss Army knife of your financial toolkit–versatile, practical, and ready for a variety of situations. Beyond the basic understanding, let’s cut to the chase: what’s the real magic behind keeping your funds liquid while earning competitive interest rates?

Let’s break it down. Liquidity in the world of MMAs means you have easy access to your funds when you need them.Need to cover an unexpected expense? No problem. Want to jump on a time sensitive investment prospect? You’re ready to go. But that is not all.

- Accessibility: write checks or make transfers with ease.

- Competitive rates: Generate more interest compared to a standard savings option.

- FDIC insured: Your money is protected, providing peace of mind.

| Feature | Advantage |

|---|---|

| Liquidity | Swift access to funds |

| Interest rates | Earn while you save |

Demystifying Money Market Account Interest Rate Fluctuations

Ever peeked at your money market account (MMA) statement and noticed the yield doing the twist? It’s not magic, but understanding the rhythm behind those fluctuations is key to maximizing your savings. Think of MMAs as finely tuned instruments, their interest rates reacting sensitively to the economic orchestra around them. The conductor? That’s often the Federal Reserve, adjusting the federal funds rate, which trickles down to influence the short-term interest rates that MMAs thrive on. Other players include prevailing Treasury yields, the overall health of the economy, and even the competitive landscape amongst financial institutions vying for your deposits. So, a booming economy might herald rising rates, while economic uncertainty could signal a downward trend.

But why does this affect you? Because a higher yield translates directly to more earnings on your saved cash! Think of it as a tug-of-war between these factors, constantly adjusting the sweet spot for your interest rate. To stay ahead, consider these factors:

- The Fed’s Moves: Keep an eye out for Federal Reserve announcements regarding interest rate policy. Many news outlets will cover this information.

- Economic Indicators: Pay attention to economic reports like inflation data and GDP growth.

- Shop Around: Compare MMA rates across different banks and credit unions regularly.

| Economic factor | Potential Impact on MMA Interest Rates |

|---|---|

| Rising Inflation | Likely Increase |

| recession Fears | Likely Decrease |

Strategic Use Cases for Money Market Accounts Beyond Emergency Funds

Think of a money market account (MMA) not just as a safety net, but a financial launchpad. Yes, their liquidity makes them ideal for emergency funds, but their potential extends so much further. Consider these alternative applications:

- Short-Term Savings Goals: Dreaming of a new gadget, vacation, or even a down payment on a car? An MMA can be a higher-yield alternative to a traditional savings account, helping you reach your goals faster.

- Tax Season buffer: Self-employed individuals or those with complex tax situations can use MMAs to set aside funds throughout the year to cover estimated tax payments or unexpected tax liabilities.

- College Savings Supplement: While 529 plans are great for long-term college savings, an MMA can be a good place to keep a portion of your college fund in a more liquid and accessible form, especially as college approaches.

- Business Opportunity Fund: Aspiring entrepreneurs can use an MMA to accumulate capital for a startup or expansion, benefiting from higher interest rates while maintaining easy access to their funds.

To illustrate, let’s say you’re saving for a few different goals. Here’s how an MMA could be strategically allocated:

| goal | Time Horizon | Money Market Allocation |

|---|---|---|

| Home Down Payment | 3 Years | $10,000 |

| Dream Vacation | 1 Year | $3,000 |

| New Business Venture | 2 Years | $5,000 |

Navigating Fees and minimum Balance Requirements for Optimal Returns

Unlocking the true potential of your money market account often hinges on understanding the fine print – those pesky fees and minimum balance requirements. Think of them as the gatekeepers to maximizing your returns. Falling below the minimum balance, for instance, can trigger a monthly maintenance fee, effectively eating into your interest gains. Or,excessive withdrawals might lead to transaction fees,especially if your account is structured to limit them. Carefully reviewing the account’s fee schedule and minimum balance policy is not just a suggestion, it’s financial self-defense! it’s like learning the operating manual for your car: understanding it will help you prevent costly damages and ensure you get the most out of your investment vehicle.

Navigating this landscape requires a strategic approach. Ask yourself: Can you comfortably maintain the minimum balance without jeopardizing your liquidity? Are there alternative accounts with lower or no fees that better align with your financial habits? Here are some elements to analyze:

- Minimum Balance Tiers: Some accounts offer tiered interest rates based on balance, rewarding higher balances with better returns – do the math to see if reaching the next tier is achievable and worth it.

- fee Waivers: Explore options for waiving fees, such as setting up direct deposit or maintaining a linked account with the same institution.

- withdrawal Limits: Understand transaction limits to avoid exceeding them and incurring penalties.

| Account Feature | Account A | Account B |

|---|---|---|

| Minimum Balance | $2,500 | $500 |

| Monthly Fee (if below min.) | $15 | $5 |

| Interest Rate (APY) | 0.50% | 0.40% |

Maximizing Your Money Market Account Strategy with Laddering Techniques

Beyond simply parking your cash, a money market account can be so much more. Ready to unlock its full potential? Imagine a carefully orchestrated climb, not a flat plateau.That’s the power of laddering. Employing this strategy in a money market involves dividing your savings into multiple “rungs,” each representing a separate account or fixed term within the same account, maturing at staggered intervals. As each rung matures, you reinvest the funds, ideally at potentially higher rates if available, or use them as needed without disrupting your entire savings strategy. this smart approach mitigates interest rate risk – the fear of locking in your funds only to see rates rise shortly after.

Why should you even consider this creative finance tactic? Let’s climb to the benefits:

- adaptability: access funds as needed when each rung matures.

- higher Potential Returns: Opportunity to reinvest at improved rates.

- Reduced Risk: Protect yourself from fluctuating interest rates.

Here’s a simplified example of a money market ladder:

| Rung | Amount | Maturity | Action |

|---|---|---|---|

| 1 | $2,000 | 3 Months | Reinvest or Use |

| 2 | $2,000 | 6 Months | Reinvest or Use |

| 3 | $2,000 | 9 months | Reinvest or Use |

Regularly evaluate your ladder and adjust terms to optimize your savings. Happy climbing!

Understanding the Tax Implications of Money Market Account Earnings

So, you’ve smartly stashed some cash in a money market account (MMA) and are watching those interest earnings tick up. Fantastic! But before you start planning that dream vacation,let’s chat about Uncle Sam. just like with savings accounts and CDs, the interest you earn from your MMA isn’t tax-free. The IRS views it as taxable income, meaning you’ll need to report it on your tax return. The good news? You typically won’t have to do any complex calculations. Banks and credit unions will send you a Form 1099-INT, detailing the total interest paid to you during the tax year. This form makes reporting a breeze. Keep in mind: the threshold for receiving a 1099-INT is generally $10.So, if you earned less than that, you technically should still report the income, but you won’t receive a form to prompt you.

Navigating the tax landscape around MMA earnings doesn’t have to be daunting. Here’s a quick rundown of key aspects to keep in mind, presented in a user-amiable format:

- Reporting Requirement: Always report your MMA interest income. It’s usually as simple as transferring data from your 1099-INT to your tax return.

- tax Form: Expect a Form 1099-INT if your earnings exceed a minimal threshold.

- Tax Bracket Influence: The rate at which your MMA earnings are taxed depends on your individual tax bracket.

- Tax-Advantaged Accounts: Consider exploring tax-advantaged accounts like IRAs or 401(k)s for other savings goals where your earnings can grow tax-deferred or even tax-free!

| Scenario | Interest Earned (Yearly) | Form 1099-INT Received? |

|---|---|---|

| Saver A | $50 | Yes |

| Saver B | $5 | No (but reportable) |

| Saver C | $500 | Yes |

Q&A

Money Market Accounts: Ask the Expert, your Future Self!

We caught up with someone who’s seen it all, navigated the finances and wished they’d started sooner… your Future Self! Get the inside scoop on Money Market Accounts (MMAs) and find out if they’re the secret ingredient your savings strategy has been missing.

Q: Alright, Future Self, you’ve been there, done that. What exactly is a Money Market Account? Sounds like somthing out of a spy novel!

A: (Chuckles softly) More like a really good savings vehicle! Think of it like a hybrid between a savings account and a checking account. You typically earn higher interest rates than a traditional savings account, while still having relatively easy access to your funds. You can frequently enough write checks and even have a linked debit card, though there might be limitations.

Q: So, it’s faster, stronger, and more profitable than a regular savings account? Does it wear a cape too?

A: (smiling) Not quite superhero status, but definitely a valuable player on your financial team! While MMAs often offer higher interest rates, they typically require a higher minimum balance to open and maintain.Think of it less like a cape and more like a tailored suit – requires a bit more investment upfront, but the long-term benefits can be significant.

Q: Okay, so who are these MMAs best suited for? The financially fearless, or the cautious savers among us?

A: Actually, they’re great for both! If you have a chunk of cash you want to grow beyond the meager interest of a regular savings account, but you might need access to it sooner rather than later, an MMA is a solid choice. Think of emergency funds, down payments, or even saving for a big vacation. It’s a cozy zone for those who are cautious but want to see their savings work harder.

Q: High yield and liquidity? Sounds almost too good to be true. What’s the catch?

A: The “catch” is more of a consideration. Interest rates on MMAs can fluctuate based on market conditions. So, while they’re frequently enough higher than traditional savings accounts, they’re not guaranteed to stay that way. Also, remember those minimum balance requirements? Falling below them often triggers fees. It’s about understanding the terms and conditions and making sure it aligns with your financial needs.

Q: Okay, Future Self, quick fire round! What are three things current-day me should consider before opening an MMA?

A: 1. Shop around! Interest rates and fees vary considerably between institutions. 2. Read the fine print! Understand the minimum balance requirements, withdrawal limits, and any associated fees. 3. Align it with your goals! Make sure it fits into your overall financial plan and helps you achieve your specific objectives.

Q: Any final words of wisdom from the future,regarding Money market Accounts?

A: (Nods thoughtfully) Don’t be afraid to take that frist step towards smarter saving. Starting small is better than not starting at all. And remember, your future self will thank you! now go forth and make those dollars work for you!

To Wrap It Up

So, there you have it. A closer look at the chameleon of the savings world, the money market account. Not quite a checking account, not quite a CD, but a financial tool that blends flexibility and potential returns in a way that can be surprisingly… well, intriguing. Whether it’s the right fit for you depends,as always,on your unique financial landscape. But armed with this knowledge, you’re one step closer to navigating the financial currents with a little more confidence, and perhaps, a little more profit in your sails. Now go, explore, and may your financial winds be ever in your favor!